Quick Summary:

- Shariah-compliant Islamic fintech app development requires an SSB-issued fatwa before code is written.

- The global Islamic fintech market reached $198B in 2024/25, growing at 11.5% annually to $341B by 2029.

- The UAE ranks third globally in the GIFT Index, with VARA, CBUAE, ADGM, and DIFC each governing different platform types.

- Core compliance is built into the architecture: halal screening engine, Islamic contract orchestration, compliant ledger, and Shariah audit trail.

- Automated Zakat, P&L distribution for Mudaraba, and Murabaha contract orchestration are distinct engineering challenges.

- Annual Shariah audits are mandatory for certification renewal and cover transaction sampling, ledger inspection, product review, and marketing review.

- A mid-tier Islamic banking platform in the UAE typically costs $150K–$350K; full-stack compliance platforms run $400K–$900K+.

As per GIFT reports, the global shariah-compliant Islamic fintech app development market hit $198 billion in 2024/25. By 2029, that figure reaches $341 billion at 11.5% annual growth, slightly faster than conventional fintech in the same geography.

The UAE ranks third globally in the GIFT Index. With VARA, CBUAE, ADGM, and DIFC each issuing active compliance frameworks for Islamic platforms, the country sits at the center of that growth.

Most platforms targeting this market fail before launch. The failure point is rarely the concept. It is the architecture.

An interest-accrual engine repurposed for profit-sharing, a contract module sequencing transactions in the wrong order, and a ledger that cannot support SSB audit requirements are not UI problems.

They are foundational engineering decisions that cannot be patched post-launch.

This post covers the regulatory map, the SSB governance process, the technical architecture, the core product modules, and the post-certification audit cycle. Everything a UAE founder building a Shariah-compliant Islamic fintech app needs before sprint zero.

Need a Shariah-compliant fintech app built for UAE regulations?

What Is Shariah-Compliant Islamic Fintech App Development?

Shariah-compliant Islamic fintech app development is the process of designing, building, and operating digital financial mobile platforms that conform to Islamic commercial law.

This requires prohibiting interest (Riba), excessive uncertainty (Gharar), and speculation (Maysir) at the architectural level, while structuring all financial instruments around real-economy asset linkage, profit-sharing, and contractual transparency.

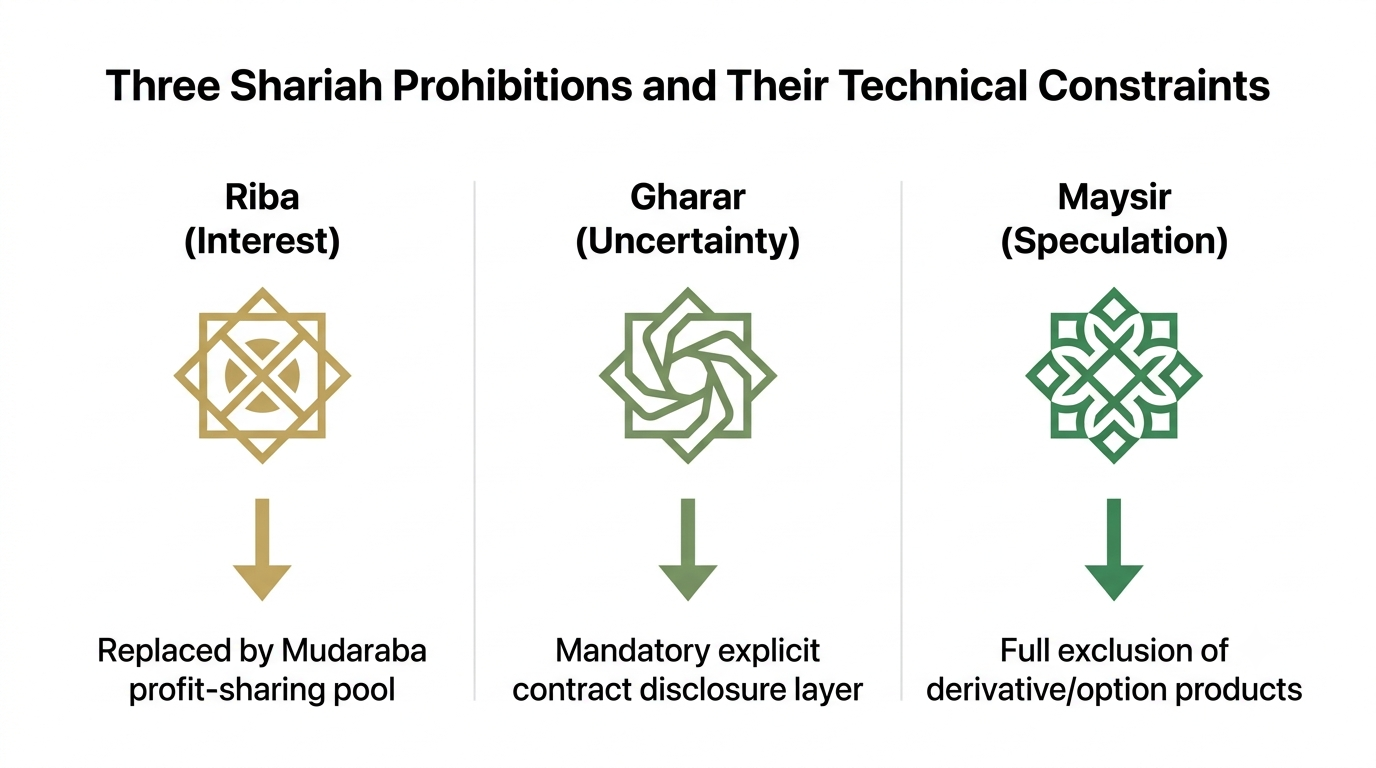

From Principle to Product — What Each Prohibition Means in Code

The three core prohibitions translate directly into engineering constraints.

Riba (Interest): A savings account cannot use an interest-accrual engine.

It must be restructured as a profit-sharing investment pool (Mudaraba). The user’s return is variable and tied to actual asset performance, not a guaranteed fixed rate.

Gharar (Uncertainty):

A financing contract must disclose the total cost, profit margin, and repayment schedule at the point of agreement.

Hidden fees, variable, ambiguous charges, or clauses that leave the final obligation open are architectural disqualifiers. Terms and conditions cannot fix them after the fact.

Maysir (Speculation):

No derivatives, options trading, or margin products with speculative exposure.

This excludes entire product categories standard in conventional fintech stacks. They are non-starters in a Shariah-compliant mobile platform.

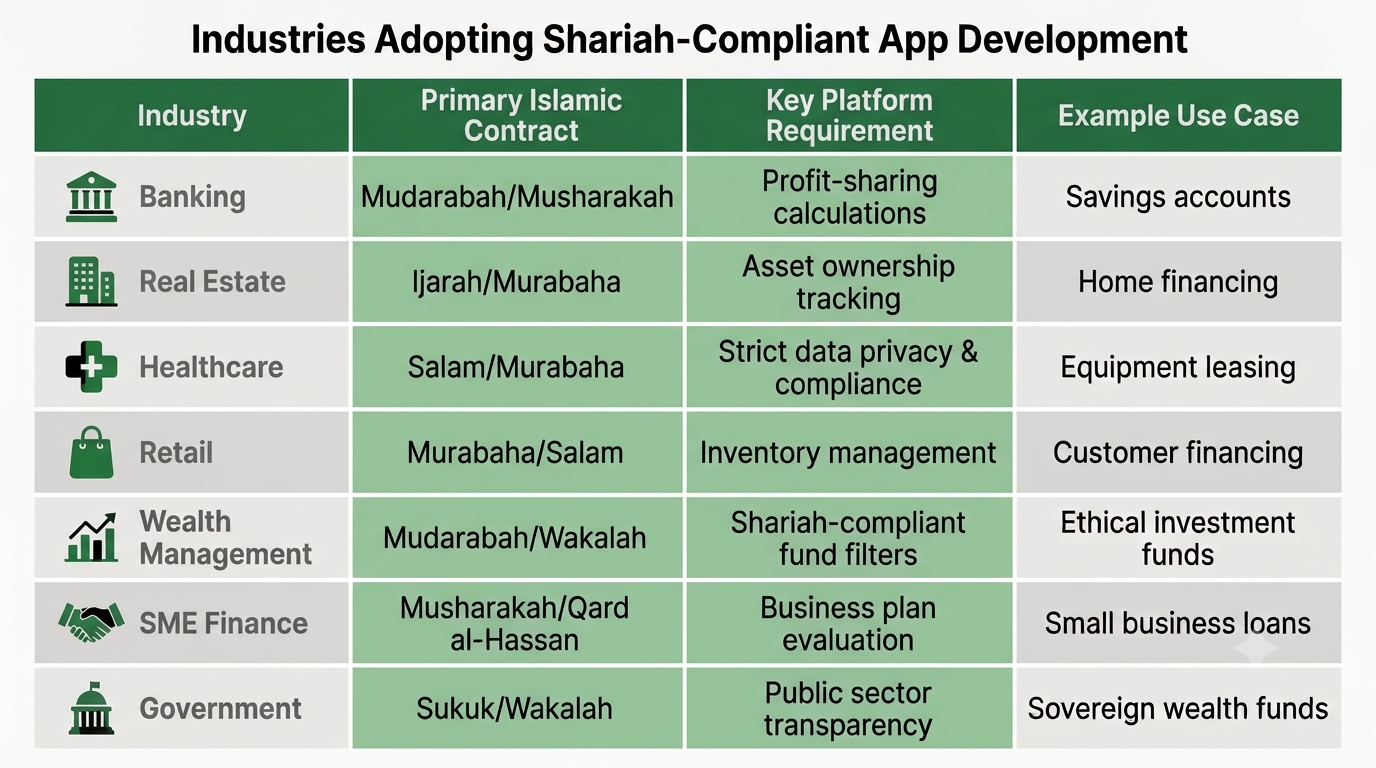

Which Industries Are Adopting Shariah-Compliant App Development?

Islamic fintech is not a banking-only discipline. Any sector with financial transactions, insurance, investment, or credit at its core has a Shariah-compliant equivalent.

In the GCC, Islamic banking assets exceed 50% of total banking assets. Demand for compliant digital mobile platforms spans the full economy, not just licensed financial institutions.

Banking and Financial Services:

The primary adopter category. Neobanks, digital wallets, and full-service Islamic banking mobile platforms all require Shariah-compliant architecture. New entrants need CBUAE licensing and full SSB governance before launch.

Real Estate and Property Finance:

UAE property runs on Ijarah (lease-to-own) and Diminishing Musharakah financing. The DLD-VARA tokenization framework (2025) opened regulated on-chain property ownership, enabling Shariah-compliant real estate investment mobile apps.

Insurance and Takaful:

Islamic insurance (Takaful) operates on mutual contribution, not premium-for-profit. Digital Takaful platforms require participant contribution pools, surplus distribution logic, and full fund separation from operator fees.

Retail and E-commerce:

Murabaha BNPL is the Shariah-compliant equivalent of buy-now-pay-later. Mobile apps serving GCC retailers must orchestrate the legal asset purchase and resale sequence, not just defer a payment.

Wealth and Asset Management:

As stated in ADIB’s press release, ADIB’s Smart Sukuk platform (launched April 2025) reduced the minimum sukuk investment from $200,000 to $1,000 through its mobile app, demonstrating a clear appetite for digital-first Islamic wealth products.

SME Finance and Crowdfunding:

Musharakah and Mudaraba equity crowdfunding mobile platforms provide Shariah-compliant capital for UAE SMEs. Profit distribution engines must activate only on actual investee returns, not scheduled payouts.

Government and Public Sector:

UAE government entities building waqf management, Zakat disbursement, and sovereign sukuk portals are direct buyers of Shariah-compliant digital mobile app systems, a procurement category that established vendors consistently underserve.

What Types of Shariah-Compliant Apps Can Be Built?

The product surface area is wider than most founders expect. Each mobile app type carries its own compliance architecture, contract type, ledger requirements, and SSB validation scope.

Islamic Banking and Neobank Apps:

Full-service current accounts, Mudaraba savings pools, card products, and payment infrastructure. The most complex build category. Requires CBUAE licensing and all four compliance architecture layers. Minimum launch timeline: 12–18 months.

Murabaha BNPL and Consumer Financing Apps:

Buy-now-pay-later structured as a cost-plus trade, not a loan. The fastest-growing Shariah-compliant mobile product category in UAE retail for 2025–2026.

Halal Investment and Sukuk Apps:

Shariah-screened equity portfolios and sukuk trading mobile apps. Require AAOIFI financial ratio screening engines and compliant profit distribution logic. Digital sukuk platforms need integration with the UAE sandbox frameworks from DFSA or FSRA.

Zakat and Sadaqah Management Mobile Apps:

Full automation requires Hijri-calendar-based asset tracking over a lunar year (hawl) and a real-time Nisab feed tied to live gold and silver prices.

Takaful (Islamic Insurance) Apps:

Participant funds must remain permanently separated from operator management fees at the ledger level, across the full policy lifecycle. This is an architectural requirement, not an accounting preference.

Equity Crowdfunding Islamic Platforms (Musharakah/Mudaraba):

Require transparent investor disclosure, including explicit loss-of-capital risk, and profit distribution engines that activate only on actual investee returns.

Waqf (Islamic Endowment) Management Platforms:

Waqf assets are legally inalienable and cannot be sold, transferred, or used as collateral. Platforms require immutable asset records and income distribution logic that permanently protects the principal endowment.

What Licenses and Regulators Apply to Islamic Platforms in the UAE?

The UAE does not have a single Islamic fintech regulator. Four bodies govern distinct product types. Operating in the wrong jurisdiction without the correct license carries fines up to AED 50 million under Federal Decree-Law No. 20 of 2018.

| Regulator | Jurisdiction | Product Types Covered |

| CBUAE (Central Bank UAE) | Federal | Digital banks, payment apps, BNPL, open banking |

| ADGM / FSRA | Abu Dhabi Global Market | Capital markets, wealth management, institutional products |

| DIFC / DFSA | Dubai International Financial Centre | Private banking, fund management, insurance |

| VARA | Dubai mainland + free zones (excl. DIFC) | Virtual assets, DeFi, tokenized sukuk, crypto-wallets |

Shariah-Compliant DeFi Protocols:

Viable under VARA’s 2026 rulebook for Dubai and the FSRA’s updated Digital Assets Framework (September 2025). The SSB must validate smart contract logic directly, not just a product concept paper.

VARA and Shariah-Compliant DeFi: The Legal Pathway

VARA (Virtual Assets Regulatory Authority) is the world’s first independent virtual assets regulator. Its 2026 VARA rulebook explicitly covers DeFi by regulating the touchpoints: platform founders, smart contract deployers, and front-end operators.

This creates a defined legal pathway for Shariah-compliant DeFi products within a regulated environment.

The DLD-VARA real estate tokenization framework demonstrates this in practice. Property ownership records are tokenized on-chain under regulatory oversight, with Islamic structures applicable to the underlying asset.

Cabinet Resolution No. 111 of 2025 expanded the definition of virtual assets to include tokenized securities and real-world asset (RWA) tokens, effective January 2026. The FSRA updated its Digital Assets Framework in September 2025 to include DeFi protocol operators with an ADGM nexus.

What Has to Happen Before App Development Starts: The SSB Process

The Shariah Supervisory Board (SSB) is the governing authority that determines whether a product is legally compliant under Islamic commercial law.

Building before SSB engagement means building on an unvalidated foundation. Architectural changes required after the build are significantly more expensive to retrofit than addressing them at design.

The SSB Structure

A Shariah Supervisory Board typically comprises three to five Islamic scholars with formal training in fiqh muamalat (Islamic commercial jurisprudence). For AAOIFI-aligned platforms, board members should hold relevant AAOIFI certification, according to AAOIFI Standards.

The Pre-Development Process: Step by Step

- The product team prepares a Product Concept Paper covering the proposed financial instrument, its economic purpose, user workflows, data flows, and ledger treatment.

- The SSB reviews this against AAOIFI standards and core Islamic commercial jurisprudence. They may require architectural changes or workflow restructuring.

- Only after the board is satisfied does it issue a fatwa, a formal ruling, for that specific product.

- The fatwa becomes the engineering blueprint the development team must implement precisely. Any deviation requires a new SSB review.

Why This Matters for Timelines

SSB engagement typically adds four to eight weeks before sprint zero. Founders who skip this step rarely save time. They spend it redesigning contract logic and renegotiating features that a scholar’s review would have caught in week one.

The Technical Architecture of a Shariah-Compliant Platform

A Shariah-compliant mobile platform is not a conventional mobile banking app with Islamic terminology applied to the interface. Compliance is structural. It lives in the contract orchestration layer, the ledger design, the screening engine, and the audit trail.

Layer 1: Halal Screening Engine

An asset and product filter that continuously checks the halal investment app’s universe against a prohibited sector list (alcohol, tobacco, conventional finance, weapons, entertainment, pork-related).

For equity platforms, the engine applies AAOIFI financial ratio screens in real time, checking debt levels, accounts receivable, and impure income percentages against permissible thresholds.

Layer 2: Islamic Contract Orchestration

This layer manages the sequencing of legal events for each Islamic contract type. Sequence matters critically.

In Murabaha, the fintech platform must take legal ownership of an asset before selling it to the user. The wrong sequence, even by milliseconds, renders the contract non-compliant. This is not conventional loan processing logic. It is a purpose-built contract state machine.

Murabaha BNPL Workflow: 5-Step Contract Orchestration

- User selects an item and requests financing.

- Fintech platform (acting as Wakala agent) purchases the item from the vendor using its own funds. The ledger records this asset transfer to establish legal ownership.

- The Islamic fintech app immediately sells the item to the user at a disclosed price (cost plus agreed profit margin), with deferred payment. This is a legally distinct second transaction.

- The system generates a digital contract disclosing total cost, profit amount, and repayment schedule. User signs electronically.

- Repayments are posted against the deferred sale balance, not against an interest-bearing loan.

The platform’s income comes from a trade transaction, not from lending money. This distinction is architecturally enforced.

Layer 3: Compliant Ledger Design

The ledger does not use interest-accrual logic. For Mudaraba investment accounts, profit distribution is calculated on actual asset performance using a separate P&L distribution module.

Each investment pool requires a segregated ledger to prevent commingling. This makes per-contract audit calculations accurate.

Layer 4: Shariah Audit Trail

Every contract state change, asset transfer, profit distribution, and purification event is recorded as an immutable, timestamped log entry.

Event-sourcing architectures are well-suited here. They produce a complete, auditable history of every step in a contract’s lifecycle, which is essential for annual SSB audit requirements.

Key Challenges in Shariah-Compliant Platform Development and How to Solve Them

Islamic fintech app development for Shariah compliance introduces engineering constraints that conventional app development in the UAE does not face. Each challenge below has a known fix.

Challenge 1: SSB Engagement Delays

A Product Concept Paper that is incomplete or technically vague adds weeks of back-and-forth before SSB approval.

Fix: Submit a technically complete document including data flows, contract state diagrams, and ledger treatment. Incomplete submissions are the primary driver of SSB delays.

Challenge 2: Sequence Errors in Contract Orchestration

In Murabaha, the legal sequence of ownership transfer is a compliance requirement, not a configuration option. A minor sequencing error in the state machine invalidates the structure.

Fix: Use purpose-built Islamic contract libraries rather than adapting conventional loan processing logic.

Challenge 3: Ledger Commingling

A single shared ledger across investment pools, standard in conventional app development, creates audit failures in Mudaraba platforms.

Fix: Architect each investment pool with a segregated ledger schema from the start. Retrofitting this post-launch is costly and audit-risky.

Challenge 4: Arabic-First UI Retrofitting

Many teams build in English first and then attempt to mirror the interface to the RTL layout. Arabic text rendering, typography sizing, and navigation hierarchy do not simply flip horizontally.

Fix: Design the Arabic interface first. Let it set the structural decisions for spacing and navigation. English can then be adapted from the Arabic baseline.

Challenge 5: Static Nisab Calculations

Zakat apps using a fixed Nisab value without a live price feed produce incorrect calculations. This is an ongoing compliance risk.

Fix: Integrate a real-time data feed for Nisab threshold values. This is a data layer requirement, not a display formatting option.

Core Product Modules Specific to Islamic Platforms

The Islamic fintech product stack includes modules with no conventional equivalent. Each requires dedicated engineering and cannot be repurposed from standard fintech libraries.

Automated Zakat Module

A complete automated Zakat feature requires four components:

Asset Tracking Engine:

Identifies and values all zakatable assets held on the platform over a full lunar year (hawl). Requires Hijri calendar integration, not a 12-month counter from account creation.

Nisab Threshold Feed:

A real-time integration pulling current Nisab values based on gold or silver prices. A static value produces incorrect calculations.

Disbursement API:

Connects to certified charitable organizations, allowing users to pay Zakat directly from the app and receive a digital receipt.

Fiqh Rules Engine:

Accommodates different scholarly interpretations of what constitutes a zakatable asset, allowing selection of the applicable school of jurisprudence.

Profit-Sharing Investment Pools (Mudaraba)

Pre-agreed profit ratios, variable return calculation, loss allocation logic, and per-pool ledger isolation. Standard yield or interest modules cannot be configured for this. A purpose-built P&L distribution engine is required.

Islamic Contract Templates

Platform-native templates for Murabaha (cost-plus trade), Musharakah (equity partnership), Ijarah (leasing), and Wakala (agency). Each template has its own state machine, legal event sequence, and documentation requirements.

Cultural and Ritual Features

Prayer time-aware push notifications, Hijri calendar integration for account statements, and Arabic-first interface logic. In GCC markets, these are trust signals, not optional product features.

Arabic-First UI/UX for Shariah-Compliant Islamic Fintech Platforms

RTL (right-to-left) layout is not a CSS toggle applied after the English design is complete. The information hierarchy, navigation patterns, icon placement, and reading flow are fundamentally different.

Arabic-first design means the Arabic experience sets the structural decisions. English is then adapted from that baseline, not the other way around.

Core Arabic UI/UX Requirements

- Layout Direction:

All content blocks, navigation menus, input fields, and icons mirror horizontally. Progress bars run right to left. Back navigation points right.

- Typography:

Arabic typefaces require larger minimum sizes than Latin equivalents at the same point size. Recommended options: Noto Naskh Arabic (web-safe, high readability) and Scheherazade (traditional forms). Line height requirements differ significantly.

- Bilingual Logic:

Arabic and English must co-exist without layout collapse. In UAE Islamic fintech, Arabic governs spacing and layout when the two conflict.

- Hijri Calendar Integration:

Account statements, contract dates, and Zakat hawl calculations require Hijri date support. This is a data layer requirement, not a display format option.

- Cultural UX Choices:

Avoid figurative human imagery in design elements. Geometric and calligraphic patterns align with the Islamic design tradition. Transaction confirmation screens can acknowledge Halal status as a trust signal.

- Prayer Time Awareness:

Suppressing non-critical push notifications during prayer times builds brand trust with observant users in GCC markets.

Need a feature specification mapped to your Islamic product type?

What Trending Technologies Are Reshaping Shariah-Compliant Islamic Fintech Apps?

The technology stack for Islamic fintech apps is changing faster in 2026 than at any earlier point. Three developments are directly shaping the Islamic fintech app development in the UAE for this space.

Tokenized Real-World Assets (RWA)

Global outstanding sukuk exceeded $1 trillion in Q3 2025 (Fitch Ratings, as cited in Arab News, February 2026. Migrating even 1% to 5% of that issuance on-chain could represent $9 billion to $45 billion in tokenized assets.

VARA’s integration with the Dubai Land Department has created a regulated pathway for on-chain property tokenization. For Islamic finance app development in the UAE targeting Islamic finance, this opens a new product category with real regulatory backing.

AI-Powered Shariah Screening

Manual halal screening of equity portfolios is too slow for real-time trading apps. AI-powered screening engines can now apply AAOIFI financial ratio thresholds across thousands of instruments in real time.

Islamic banking apps are beginning to use LLMs to pre-check contract documentation against known fatwas before SSB submission. This reduces SSB review cycles without replacing the scholar’s formal ruling.

Stablecoins as Settlement Infrastructure

Combined stablecoin market capitalization reached approximately $317 billion in early 2026, as per GIFT Report 2025/26, by DinarStandard & Elipses. For Islamic finance, asset-backed and commodity-linked stablecoins offer a Shariah-compatible settlement mechanism.

Cross-border Murabaha transactions using stablecoins reduce settlement time from days to minutes, a practical advantage for UAE mobile platforms serving OIC markets.

Blockchain for Waqf and Zakat

Waqf platforms require immutable asset records by definition. Waqf assets cannot be transferred or liquidated, and blockchain provides a permanent audit record that aligns with this structural requirement.

Several UAE government entities are piloting blockchain-based Zakat disbursement platforms to track fund movement from payment to beneficiary, improving transparency across the full Zakat cycle.

Shariah Certification and the Annual Audit Cycle

Getting the initial Shariah compliance certificate marks the beginning of a recurring governance commitment, not its end. Annual certification renewal requires a structured SSB audit.

Passing it consistently separates compliant mobile platforms from those with nominal Islamic branding.

The Initial Certification Process

After development is complete, the SSB reviews the implemented product against the original fatwa. This review typically takes four to eight weeks. If the implementation matches the approved blueprint, the board issues a Shariah Compliance Certificate.

If changes occurred during development, the review restarts from that change point.

The Annual Audit Cycle: Four Components

Transaction Sampling:

A statistically significant sample of transactions is reviewed to confirm the executed contract logic matches the approved fatwa. Minor sequence deviations require remediation.

Ledger Inspection:

Verification that profit distribution ratios are applied correctly, non-compliant income has been purified (donated to charity), and Zakat calculations are accurate.

Product Review:

All new features or product changes since the last audit are assessed against existing fatwas. New product types require new fatwas before launch, not after.

Marketing and Communications Review:

All external content claiming Shariah compliance is reviewed for accuracy. Misrepresentation, intentional or not, is a certification risk.

Failing the annual audit results in loss of certification. Platforms that maintain consistent certification across multiple cycles build a structural credibility advantage that new entrants cannot replicate with marketing spend.

How Much Does It Cost to Build a Shariah-Compliant Islamic Fintech App in the UAE?

Build cost is driven by compliance complexity, not feature count. Two fintech apps with identical user-facing features can differ by 300% in development cost if one requires full SSB governance, Mudaraba P&L architecture, and VARA licensing while the other does not.

Cost Ranges by Platform Type

| Platform Type | Estimated Cost | Timeline |

| Single-module MVP (Zakat calculator, halal screening) | $30,000–$60,000 | 3–5 months |

| Mid-tier Islamic banking app (1–2 contract types, SSB) | $150,000–$350,000 | 6–10 months |

| Full-stack platform (Murabaha + Mudaraba + Zakat + audit trail + SSB) | $400,000–$900,000+ | 10–18 months |

UAE-Specific Cost Factors

- VARA licensing: AED 50,000–AED 370,000 depending on license category and activity type

- SSB retainer: $3,000–$10,000/month, depending on board composition and review frequency

- Hijri calendar API and Arabic localization: $15,000–$40,000 as a standalone component

- Annual Shariah audit: $20,000–$60,000 per audit cycle

Recommended Tech Stack

- Mobile: React Native or Flutter (both support RTL layout natively)

- Backend: Node.js with an event-sourcing architecture for the Shariah audit trail

- Ledger: PostgreSQL with an isolated schema per investment pool (prevents commingling)

- Screening API: AAOIFI-aligned data providers such as Refinitiv or IdealRatings

How Code Brew Labs Builds Shariah-Compliant Islamic Fintech Apps

Code Brew Labs has 13 years of experience in mobile application development across fintech, enterprise, and regulated industries. Our case studies show the methodology in practice.

Alfardan Exchange | Fintech

Code Brew Labs built a fast, compliant remittance platform for one of the UAE’s largest exchange houses. The platform handles real-time international transfers with full regulatory compliance and a transaction experience built for high-frequency expat use.

Results: 100K+ user downloads | 99.9% platform uptime | 3-second average transfer speed

duPay | Fintech

A UAE-regulated digital wallet and cross-border transfer app for the region. Built with a compliant transaction infrastructure and an interface designed for simplicity in daily use.

Results: 100K+ user downloads | 99.9% transaction success rate | 4.7 App Store rating

Both platforms were built with regulatory compliance built into the architecture, not added as a post-launch patch. That same methodology applies directly to Shariah-compliant Islamic fintech app development in the UAE.

For founders evaluating fintech app development in the UAE for Islamic finance, Code Brew Labs offers a pre-build consultation. The scope covers SSB engagement readiness, architecture planning, and regulatory pathway selection before a line of code is written.

Conclusion:

Shariah-compliant Islamic fintech app development is a specialized discipline. The platforms that succeed in the UAE’s Islamic fintech market are not the ones with the most Islamic features on the surface.

They are the ones where the SSB engaged before sprint zero, the contract orchestration layer was built to the correct legal sequence, the ledger was architected for Mudaraba P&L distribution, and the annual audit cycle was built into the operating model from launch.

The GIFT Report 2025/26 is clear: the market is moving from experimentation to execution. The UAE is at the center of that shift.

Founders who start with the architecture get to market faster and stay compliant longer.

FAQs

Q1: What makes an app Shariah-compliant?

A Shariah-compliant app must prohibit interest (Riba), excessive uncertainty (Gharar), and speculation (Maysir) at the architecture level, not just in the terms and conditions. This means compliant ledger design, Islamic contract orchestration (Murabaha, Mudaraba, Musharakah), halal asset screening, and SSB-issued validation before launch. Compliance is an engineering discipline, not a marketing label.

Q2: Do I need a Shariah Supervisory Board before I start building?

Yes. The SSB reviews your Product Concept Paper and issues a fatwa before development begins. This fatwa becomes the binding engineering blueprint. Building without SSB validation means building on an unvalidated foundation. Architectural changes required after the fact cost significantly more than addressing them at design. (Source: AAOIFI Standards, aaoifi.com)

Q3: Is DeFi allowed under Islamic finance in the UAE?

Yes, within a regulated framework. VARA’s 2026 rulebook explicitly covers DeFi, regulating the touchpoints: founders and front-end operators, rather than banning the technology. This creates a legal pathway for Shariah-compliant DeFi products such as asset-backed tokenization and profit-sharing liquidity pools structured as Musharakah. (Source: VARA Rulebook, vara.ae/rulebook)

Q4: How long does it take to get Shariah certification in the UAE?

From initial SSB engagement to receiving a Shariah Compliance Certificate typically takes four to six months for a standard product. This includes the Product Concept Paper review (four to eight weeks), development with SSB oversight, and a final product review (four to eight weeks). More complex platforms with multiple contract types or novel DeFi structures can take eight to twelve months.

Q5: What is the difference between Murabaha and a conventional loan?

In a conventional loan, the lender provides money and earns income through interest. In Murabaha, the platform purchases an asset outright, takes legal ownership, and then sells it to the buyer at a disclosed cost-plus price with deferred payment. The platform’s income is a trade margin on a real asset sale, not interest on borrowed money. The legal ownership transfer is what makes the structure compliant.

Q6: How is the future of Islamic finance shaping digital products?

Global outstanding sukuk exceeded $1 trillion in Q3 2025 (Fitch Ratings). Stablecoin market capitalization reached approximately $317 billion in early 2026 (GIFT Report 2025/26). Tokenized real-world assets and AI-powered halal screening are moving from pilot projects to production infrastructure. VARA, CBUAE, and ADGM are all actively adapting their frameworks to support digital Islamic finance products.

Q7: What do support, maintenance, and post-launch services look like for a Shariah-compliant platform?

Post-launch, a Shariah-compliant platform requires ongoing SSB engagement for any product changes, an annual audit cycle covering transaction sampling and ledger inspection, and continuous Nisab feed maintenance for Zakat modules. Any new product type requires a new fatwa before launch. Annual audit costs typically run $20,000–$60,000, depending on platform complexity.

Let's Convert Your Business Idea Into Success!

Free Consultation from Top Industry Experts

Let’s Build Your Dream App!

Share article on :